#Cyber Security

What Is Continuous Assurance in Cybersecurity?

Organizations invest heavily in security tools, compliance programs, and risk management processes. Yet many security leaders still struggle...

Banks today operate in a high-stakes environment, managing sensitive financial data, digital customer interactions, and a growing portfolio of online services. These innovations, while necessary, have dramatically increased their exposure to cyber threats.

A single data breach can erode customer trust, disrupt operations, and invite severe regulatory penalties. That’s why cybersecurity risk assessment in banking has become essential—not just for compliance, but for resilience.

Unlike generic IT risk frameworks, a banking-specific risk assessment must account for sector-specific factors such as:

At the heart of this process lies the risk assessment matrix—a tool that helps institutions visualize and prioritize cyber threats based on likelihood and impact. When integrated into an actionable risk register and broader enterprise risk assessment strategy, it becomes a catalyst for informed decision-making.

This guide explores how banks can design and implement a cybersecurity risk matrix tailored to their unique challenges. We’ll cover the types of risk most relevant to banking, offer templates, and share insights on aligning risk assessments with enterprise-level goals and compliance obligations.

The financial sector is a prime target for cybercriminals—and for good reason. Banks manage high-value assets, handle massive volumes of sensitive customer data, and provide access to critical infrastructure like payment networks and credit systems. A single vulnerability can have cascading effects not only on the institution itself but also on the broader economy.

Cyber threats against banks have evolved far beyond rudimentary phishing scams. Today, they include:

In 2024 alone, global financial institutions faced billions in losses due to cyber incidents—underscoring the urgent need for proactive risk management.

Governments and financial regulators have responded with stringent cybersecurity mandates. Depending on your jurisdiction, your cybersecurity risk assessment must align with one or more of the following:

The RBI has issued several mandates to strengthen cybersecurity and enterprise risk management in the banking sector:

SEBI’s cybersecurity framework applies to banks involved in capital markets, mutual funds, and depository operations. Key guidelines include:

These mandates necessitate structured cybersecurity risk matrices tailored to specific financial operations—whether it’s lending, trading, or fund management.

Indian banks operating internationally, or those integrated with global systems like SWIFT, must also align with broader enterprise risk management standards:

A well-structured cybersecurity risk assessment must begin with a thorough understanding of the different types of risk unique to financial institutions.

Below are the most critical categories to include in your risk assessment matrix, particularly when aligned with RBI, SEBI, ISO 27005, and NIST frameworks.

Phishing emails, SMS scams, and voice fraud (vishing) are commonly used to trick employees or customers into revealing credentials or initiating fraudulent transactions. Banks are frequent targets due to their direct access to funds and sensitive data.

Malware injected into ATMs or point-of-sale terminals can intercept PIN data or manipulate withdrawal commands.

Attackers may exploit vulnerabilities to gain unauthorized access to banking systems, often through compromised admin credentials or insecure APIs.

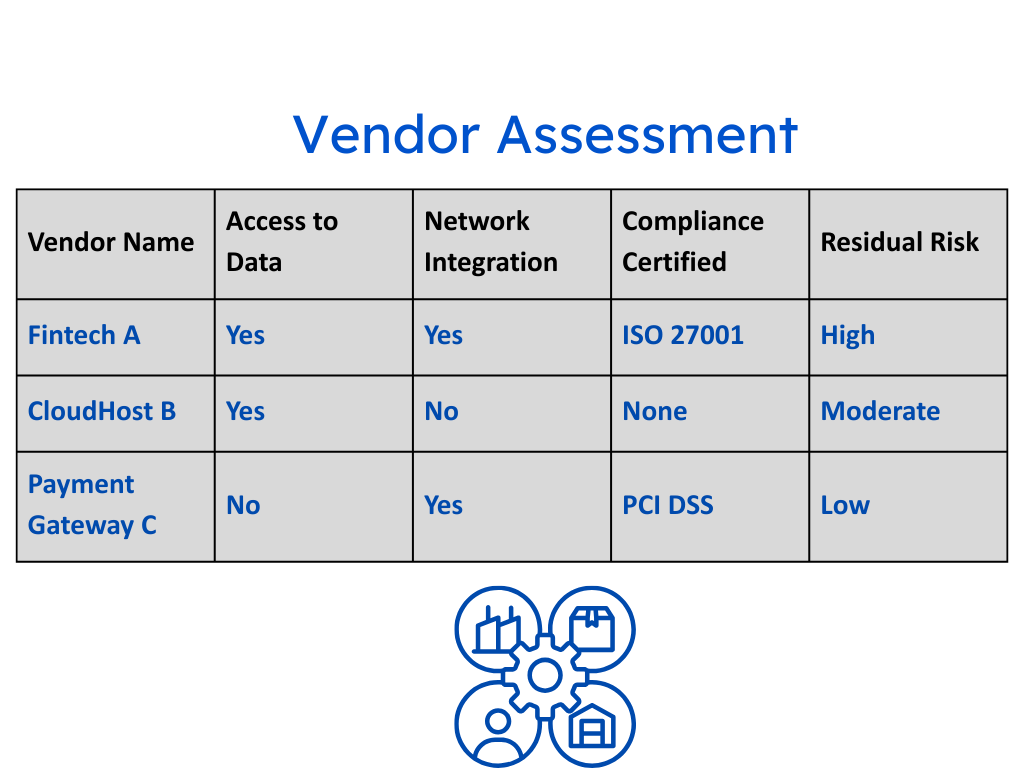

Banks often depend on third-party vendors for payment gateways, KYC processing, or cloud services. Any security flaw in these integrations can expose core systems.

DDoS attacks aim to flood online banking platforms with traffic, rendering them inaccessible and disrupting customer transactions.

Not all threats are external. Employees or contractors with legitimate access can intentionally or accidentally leak customer or transactional data.

Attackers can encrypt banking databases and demand ransom payments to restore access, potentially halting business operations.

Failure to assess and mitigate cyber risks can lead to non-compliance with RBI/SEBI mandates, ISO standards, or global requirements like GDPR/SWIFT CSP.

Each of the above risks should be evaluated in a risk assessment matrix based on:

This prioritization allows banks to channel resources effectively—focusing on the most pressing threats while maintaining a holistic enterprise risk management view.

This structured approach ensures that cybersecurity is embedded into your bank’s day-to-day governance—making audits smoother, decisions smarter, and operations more secure.

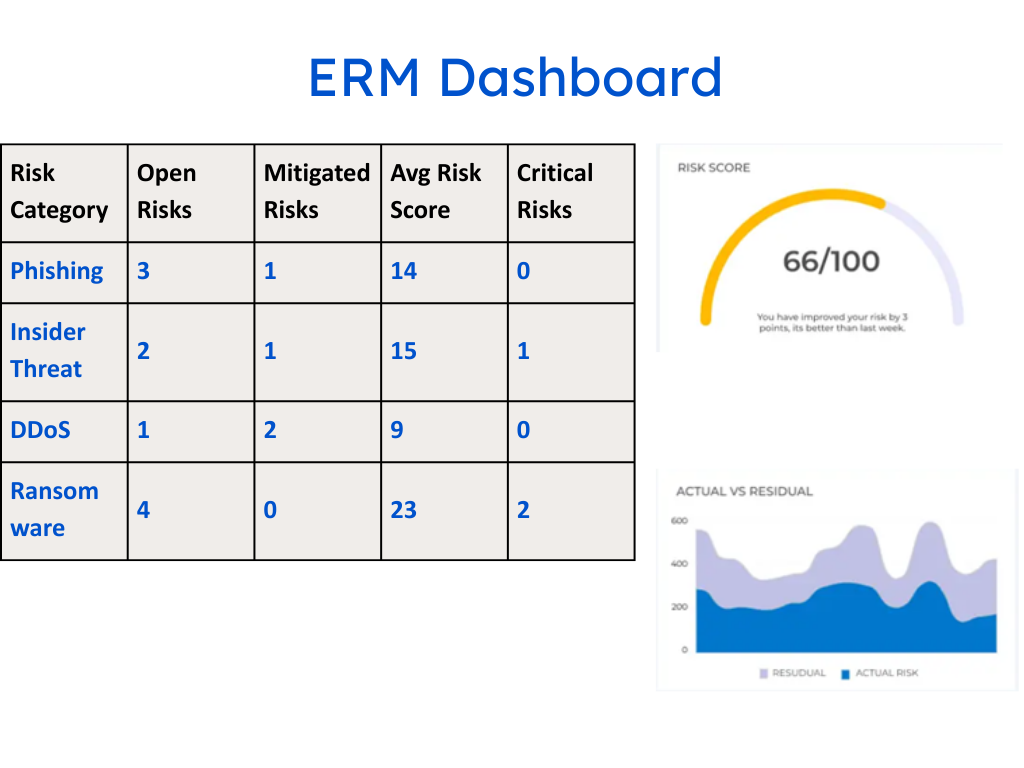

Creating a risk assessment matrix is only the first step. To truly operationalize cybersecurity within a bank, those matrix insights must flow into a risk register and align with a broader enterprise risk management (ERM) strategy. This integration ensures that cybersecurity risks are not treated in isolation but are managed alongside financial, operational, strategic, and compliance risks.

Let’s explore how banks can build this integration for scalable, auditable, and board-level risk visibility.

A risk register is a centralized, living document or platform that captures:

For cybersecurity, each row in your register should correspond to a risk highlighted in your matrix. This ensures continuity between identification, prioritization, and treatment.

Regulators such as RBI (via the Cybersecurity Framework) and SEBI (via Cyber Resilience Guidelines) mandate structured documentation of cyber threats, incidents, controls, and mitigation plans. A well-maintained risk register fulfills this obligation and serves as a ready tool during audits or supervisory reviews.

An enterprise risk assessment looks at all major risk domains under a unified framework. For cybersecurity risks to get the attention and resources they deserve, they must be embedded into this enterprise view.

For banks with extensive operations, managing this process manually can be error-prone. Consider tools that offer:

| Benefit | Impact |

| Regulatory Readiness | Smooth audits, reduced compliance risk |

| Enterprise-Wide Risk Visibility | Informed strategic decisions by the board and CXOs |

| Faster Response & Recovery | Clear ownership and pre-defined mitigation protocols |

| Reduced Operational Silos | IT, legal, and business units collaborate on cyber risks |

When integrated correctly, your risk assessment matrix becomes the foundation for a dynamic, responsive, and enterprise-wide risk management system.

Real-world incidents offer powerful lessons in the importance of proactive cybersecurity risk assessment. Below are notable cyberattacks on banks—both in India and globally—that highlight what can go wrong without a robust risk assessment matrix and risk register in place.

Type of Attack: Malware and SWIFT compromise

Loss: ₹94 crore (~$13.5 million) siphoned off in two days

What Happened:

Hackers breached the bank’s internal systems and bypassed authentication mechanisms to fraudulently authorize SWIFT transfers and ATM withdrawals across multiple countries.

Missed Risk Factors:

Risk Matrix Insight:

This incident would have scored Critical on both likelihood and impact if the matrix had modeled SWIFT fraud risk properly. Proper mapping to the risk register could have enabled stronger third-party isolation and transaction control.

What Happened:

An ATM managed by a third-party vendor was found to be infected with malware that copied user card data and PINs. These were then used for unauthorized withdrawals.

Missed Risk Factors:

Risk Matrix Insight:

A well-defined third-party risk matrix could have flagged vendor-managed ATMs as high-risk assets. Assigning ownership and implementing DLP measures would have prevented or reduced the breach impact.

Type of Attack: Cloud misconfiguration & insider threat

Data Breached: 100 million customer records

What Happened:

A former employee exploited a vulnerability in a misconfigured AWS firewall, gaining access to sensitive data stored in the bank’s cloud environment.

Missed Risk Factors:

Risk Matrix Insight:

A mature enterprise risk assessment would have modeled cloud service risks as high-likelihood, especially in hybrid architectures. Tracking such risks in a central risk register with controls around IAM and data governance would have reduced exposure.

| Lesson | Why It Matters |

| Visibility across all IT and third-party assets | Unseen assets are unmanaged and unprotected |

| Risk ownership and response clarity | Lack of accountability leads to response delays |

| Continuous reassessment | Static matrices miss evolving threats like zero-days and insider tactics |

| Risk-to-business mapping | High-impact risks often don’t seem technical—until they hit core revenue streams |

These cases underscore a critical truth: cybersecurity risk assessments must be living, adaptive processes, not annual check-the-box exercises. A regularly updated risk assessment matrix, integrated with an active risk register and monitored by a cross-functional team, is the only way to stay ahead of adversaries in banking.

To translate strategy into execution, banks need ready-to-use, customizable templates that embed cybersecurity into daily operations and regulatory reporting. These templates should support the visualization, prioritization, and tracking of cyber risks—while aligning with RBI, SEBI, and global frameworks such as ISO 27001, NIST CSF, and SWIFT CSP.

Below are key templates every bank should consider to operationalize its risk assessment matrix and enterprise risk management (ERM) practices.

Features:

Use Case: Helps visualize high-impact cybersecurity threats and drive prioritization.

✅ Regulatory Fit: Aligns with RBI Cyber Security Framework and SEBI’s risk-tiered controls.

Features:

Use Case: Ideal for internal audits, IT governance reviews, and board presentations.✅ Regulatory Fit: Satisfies documentation mandates from RBI and SEBI for internal cybersecurity posture reporting.

Features:

Use Case: Provides risk committees and CXOs with a birds-eye view of evolving risk exposure.

✅ Regulatory Fit: Maps to Basel Committee recommendations on ERM integration.

Features:

Use Case: Helps banks secure fintech integrations, outsourced IT services, and API providers.

✅ Regulatory Fit: Supports SEBI’s intermediary oversight and RBI’s third-party risk guidelines.

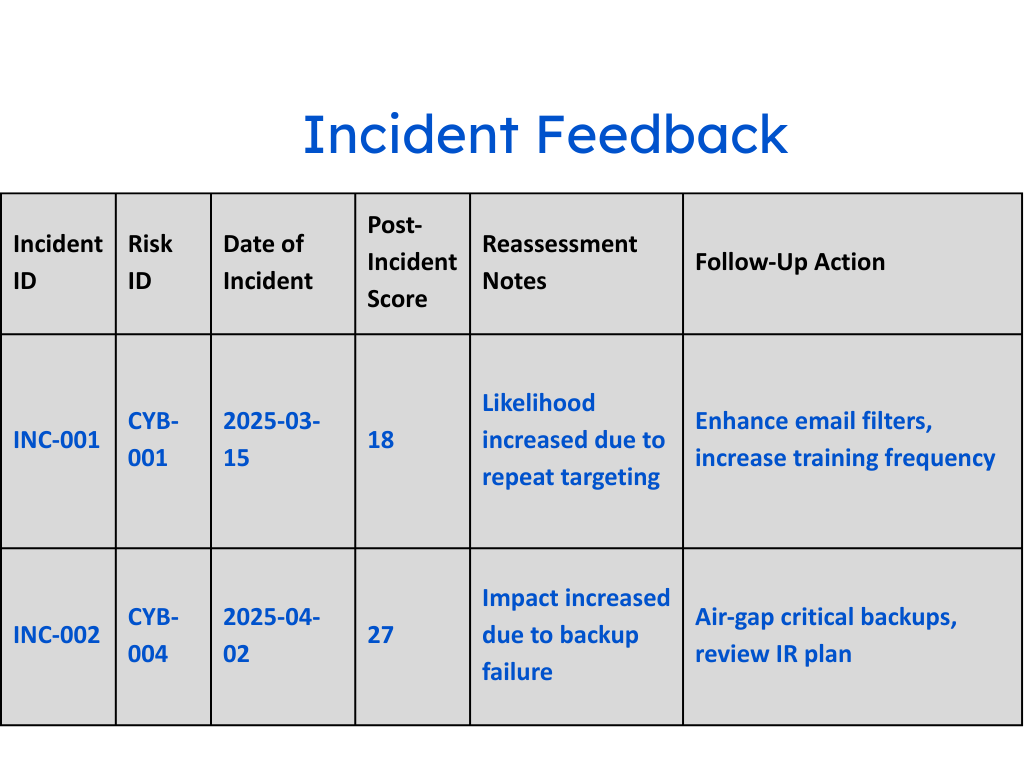

Features:

Use Case: Ensures dynamic updates to the matrix post-cyber events.

✅ Regulatory Fit: Meets RBI’s requirement for cyber incident learnings to be reflected in internal risk frameworks.

💡 Pro Tip: Maintain version history of all templates for audit purposes and link risk registers to incident logs for traceability.

As banks face increasingly complex threats, a static checklist is no longer sufficient. They need a dynamic, actionable approach to cyber risk—one that integrates seamlessly into broader enterprise risk management strategies.

The cybersecurity risk assessment matrix plays a vital role in this transformation. By helping banks visualize, prioritize, and respond to a wide range of cyber threats—from phishing and ransomware to insider threats and cloud misconfigurations—it empowers teams to act before damage is done.

But the matrix is just the starting point.

…these are the practices that separate reactive institutions from resilient ones.

The templates we’ve provided can help your organization take that leap—from compliance to competence. Whether you’re preparing for an RBI cyber audit, planning your next internal security drill, or presenting risk exposure to the board, these tools will help you deliver not just data—but decisive action.

In banking, cybersecurity risk isn’t just IT’s problem—it’s everyone’s priority. Equip your team with the frameworks, templates, and insights they need to protect your institution and your customers.

Organizations invest heavily in security tools, compliance programs, and risk management processes. Yet many security leaders still struggle...

Introduction — When the Cloud Shakes, Compliance Crumbles When AWS’s US-east-1 region went dark, so did thousands of...

Introduction There are two sides to a coin and AI is no exception. AI’s versatility is what makes...